A tax break promised to millions is now being filtered through a narrow definition that is creating confusion, delays, and political risk.

What to Know

- The promise was simple: no tax on tips, but many workers are finding eligibility depends on job classification and how their income is reported

- Workers in clearly tipped roles, including stylists and other service providers, are discovering their income does not always qualify

- Common practices like automatic service charges often do not count, leaving workers without the expected benefit

- Employees working side by side in the same business can face different tax outcomes, creating a visible fairness issue

- Small business owners are now responsible for navigating complex rules and explaining unequal results to their staff

Enactment of the One Big Beautiful Bill Act on July 4, 2025 was anchored by a clear promise: no tax on tips. For millions of service workers, this represented rare, direct financial relief. As policy transitions from campaign messaging to IRS implementation, a more constrained reality is emerging. The IRS is not just administering tax relief. It is determining which workers qualify.

The law was framed broadly, but implementation has been defined through a narrow administrative lens. By tying eligibility to predictable and historically recognized tipping patterns under the TTOC framework, administrative agencies have created a clear divide within the workforce. This classification bottleneck marks a point where policy intent diverges from administrative reality, creating immediate economic and political tension.

The Classification Gap: Included vs. Excluded

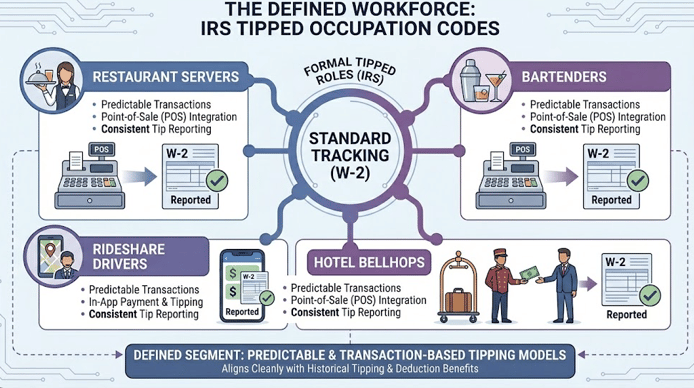

The IRS has formalized the Treasury Tipped Occupation Code system, establishing a defined group of roles that meet the standard of “customarily and regularly” receiving tips. Included roles are predictable and transaction-based: restaurant servers, bartenders, rideshare drivers, hotel bellhops. These workers align cleanly with historical tipping models and represent primary beneficiaries of the deduction.

Outside that definition sits a much larger and more structurally complex segment of the workforce. The personal care sector alone includes over 1.3 million workers in the United States, many of whom receive tips as a meaningful share of income but through inconsistent or hybrid structures. Nail technicians, hair stylists, and barbers often operate within commission-based models where tipping exists but is not uniform or separately tracked.

Hospitality support roles add another layer of complexity. In full-service restaurants and resorts, tip pooling can account for 20%–40% of total tip distribution, yet workers receiving pooled income may lack direct attribution required under current rules. As a result, workers participating in the same service experience can face different eligibility outcomes.

Understanding the Gig Environment

In platform-based and gig environments, classification becomes even more fragmented. More than one in three U.S. workers now participate in some form of gig or nontraditional work, where compensation structures vary widely. When tips are labeled as incentives, bonuses, or platform-driven adjustments rather than direct gratuities, identical economic activity produces different tax outcomes.

|

A gig refers to short-term, flexible work performed on a task-by-task or project basis rather than through a traditional, long-term employment relationship. |

Workers performing comparable services often face disparate eligibility outcomes based on legacy classification frameworks rather than actual tipping income. As tipping behavior expands, static administrative definitions create structural inconsistencies that fail to reflect modern service compensation practices.

The Fine Print Reality

Early reaction to the policy was overwhelmingly positive. Workers expected a simple outcome: keep more of what they earn. In practice, that expectation is colliding with a more complex reality. Some workers are already expressing frustration that “no tax” does not apply to payroll taxes like Social Security and Medicare, and that eligibility depends on how their job is classified.

“I voted for this because I thought ‘no tax’ meant my whole tip was mine… It feels like a bait-and-switch.”

— Summary of worker sentiment from early 2025 filing discussions

At the same time, others are still seeing meaningful benefits. A Nevada server testified that the policy effectively offsets a year’s worth of household energy costs, while a DoorDash driver said it would allow her to spend more time with family. That split reaction is the core issue. The policy is working clearly for some workers, while creating confusion or exclusion for others doing similar work.

The Employer Bottleneck: Where Policy Hits Operations

If workers are experiencing inconsistency, employers are absorbing the complexity. Small business owners broadly support the intent of the policy. In many cases, it has improved hiring conditions, particularly in front-of-house roles where untaxed tip income is now a stronger incentive. But that upside is being offset by a growing administrative burden.

What was communicated as a simple tax break has translated into a classification and reporting challenge at the payroll level. Many owners describe a shift from policy support to operational strain as they work through IRS definitions of what qualifies as a tip versus a service charge. The distinction is not cosmetic. It determines tax treatment, reporting requirements, and potential audit exposure.

“I’m all for my staff keeping more of their money… But the IRS guidelines on what is a ‘qualified tip’ versus a service charge are 40 pages long… If I get it wrong, I’m the one the feds come after.”

— Summary of small business owner sentiment during the 2026 filing season

That pressure is reinforced by formal reporting requirements. Employers must now track and report both cash and non-cash tips alongside employee occupation codes on Form W-2, while navigating exclusions across entire industries.

“Employers will need to report the total amount of cash and non-cash tips reported by an employee and the occupation of the employee on the employee's Form W-2... certain fields—healthcare, athletics, and the performing arts—are specifically carved out.”

— Ogletree Deakins Legal Analysis, July 2025.

At the same time, internal workplace dynamics are shifting. Owners are managing growing tension between tipped and non-tipped staff, as tax advantages apply unevenly across roles operating within the same business. External analysis reinforces that concern. The Economic Policy Institute has warned the policy may put downward pressure on base wages, while tax experts argue the structure creates uneven treatment across workers in similar roles.

Interpreting the Classification Landscape

Disparities are highly visible at the workplace level where, within a single property, one role may qualify while another operating within the same service environment does not. These inconsistencies are easily understood by workers and consumers alike, creating a simplified fairness narrative that is difficult to counter once established.

|

2026 Tipped Income Federal Qualification Matrix |

||||

|

Category |

Primary Worker Types (IRS Codes) |

Tip Collection Method |

Qualification for $25k Deduction |

Risk/Audit Focus |

|

Gold Standard (Directly Tipped) |

Servers (331), Bartenders (332), Bellhops (301), Valets (801), Rideshare Drivers (802) |

Direct & Voluntary: Paid via cash, credit card, or app without negotiation. |

High (The primary target for the OBBBA deduction). |

Low: Safe if reported on W-2 or 1099. |

|

Personal Services (New Expansion) |

Barbers (603), Manicurists (605), Fitness Instructors (608), Tattoo Artists (609) |

Hybrid: Often involves a mix of service commission + voluntary gratuity. |

Moderate to High (Now explicitly included in 2026 list). |

High: Risk of mixing "Service Commission" (taxable) with "Tip" (deductible). |

|

Pooled/Indirect Structures |

Bussers & Runners (102), Somme-liers (102), Back-of-House (105/106) (if no tip credit is taken) |

Distribution-Based: Tips collected by one and redistributed via payroll. |

Moderate (Qualified if voluntary from the customer). |

High: IRS scrutiny on whether managers/supervisors illegally "dipped" into the pool. |

|

Platform-Based Gig Work |

DoorDash (804), UberEats(804), Instacart 804), TaskRabbit (401) |

Digital Triggers: Tips often prompted after service or during checkout. |

Variable: Must be reported on 1099-K/NEC to qualify. |

Moderate: Difficulty in separating "Incentive Bonuses" from "Customer Tips." |

|

Service Charge (Excluded) |

Banquet staff (102), Large party servers (6+ people) (102), Room Service (103) |

Mandatory/Automatic: Set by the house (e.g., 18% auto-gratuity). |

Low/None: Classified as "Wages," not "Tips" by the IRS. |

Low: Employer usually handles withholding correctly. |

|

Professional/SSTB (Ineligible) |

Freelance consultants, Accountants, Theater Singers (206) |

Gratuity for specialized skill: Tips given for "expert" performance. |

None: Excluded under "SSTB" (Specified Service Trade or Business) rules. |

High: Attempts to reclassify fees as tips will trigger audits. |

The framework above reflects finalized IRS guidance, which makes clear that eligibility is not determined by whether workers receive tips, but by how those tips are structured, recorded, and classified within established reporting systems.

Alignment is strongest in traditionally tipped occupations, where compensation flows directly from customer to worker without intermediary complexity and conforms to longstanding definitions of gratuity. Outside this core group, classification becomes progressively less stable. Personal service occupations and hybrid compensation roles introduce variability in how income is earned and reported.

In these environments, tipping is often embedded within commission-based or bundled pricing models, making it difficult to isolate what qualifies as a deductible tip versus standard compensation. This creates elevated compliance risk not because tipping is absent, but because it is not consistently defined.

Wrap Up

The core challenge is not legislative intent, but alignment between policy design and real-world compensation structures. Current implementation relies on narrow classification standards that do not fully capture how tipping functions across large segments of the modern service economy. As a result, workers performing comparable roles can experience materially different outcomes based solely on how their income is structured, recorded, or attributed within existing systems.

This has introduced a measurable fairness gap while increasing compliance ambiguity for employers and enforcement complexity for regulators. Risk is not isolated to edge cases. It is concentrated in expanding portions of the workforce where tipping is present but does not conform to legacy definitions. In these environments, classification becomes the determining factor of eligibility, rather than the presence or significance of tipped income itself.

Policy has been implemented, but distribution of its benefits remains uneven. Moving forward, the central issue is not whether tax relief exists, but whether its structure aligns with how income is actually earned across the workforce. That alignment will determine both operational stability and how the policy is ultimately understood by workers, employers, and the broader public.